Our beautiful minds are badly illogical sometimes. We buy three cases of Cactus Cooler we don’t need because it’s on sale. We remit tax dollars instead of redlining our IRAs. And we miss owning the classic Corvette of our dreams because it “costs too much.” Say what?

There’s really no such thing as paying too much for a classic Corvette, and I think I can prove it to you.

Must pay to play

People often fret about whether they’ll make money on their classic-car purchase. “The guy wants $24k, but after doing the brakes, hoses and fluids, plus shipping, tags and insurance, I’ll be in it $30k,” goes the refrain. “And that’s all those are worth.” I’m chiding myself here because I’ve been that guy, sitting on the fence worrying about whether a car that’s supposed to be fun is a good deal. A particularly sore point is the 4-speed GTO convertible that got away. But that’s another tale. …

Let’s explore the illogical part. Collector cars are definitely fun, the same way dinner and drinks out with friends, a movie and popcorn with your significant other, and a fishing or golf weekend are fun. Do we quibble about these things costing money? No. Instead, we are pragmatic about it — we plan ahead and accept that you gotta pay if you wanna play. Buy the ticket, take the ride.

How used beats new

Used cars, particularly classics such as Corvettes, are almost invariably a great deal compared to new ones. And here’s the proof. The ACC Premium Auctions Database has a terrific graphing data feature that lets you project the value of a particular year, make and model (even including engine, transmission and other features) over a given period. Its purpose is to help you understand how a car’s value has changed over time, and that can help you estimate how much a certain vehicle will cost you — or potentially make for you — in the future.

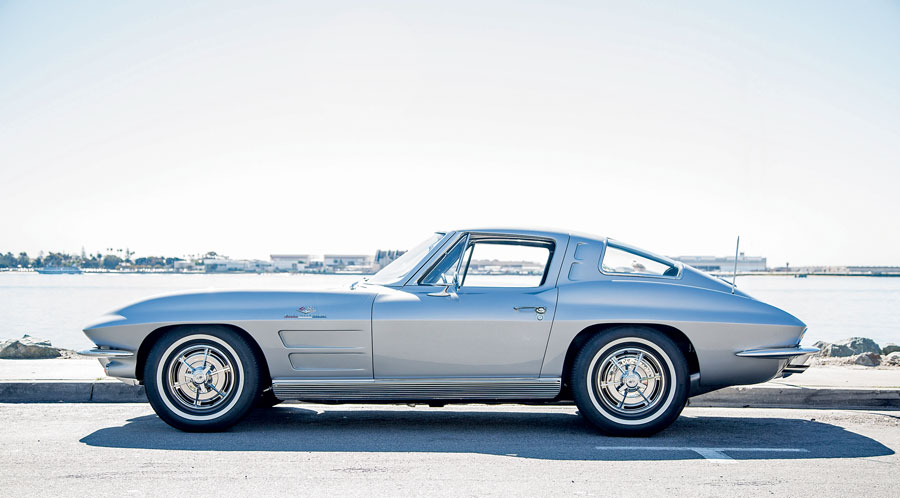

ACC Auction Editor Chad Tyson ran a comparison illustrating how, value-wise, a used mid-year Sting Ray compares with a late-model Corvette over the same period. Instead of looking forward, which would only provide a projected comparison, Chad stepped back in time to 2013 and then indexed forward to 2016, showing what actually did happen to the values of these cars over approximately three years. His chart below compares the value trajectory of a 1963 fuel-injected coupe purchased for $116,600 in 2013 to the value trajectory of a 2013 Z06 coupe purchased for $75,600 at the same time, forwarding to today. (Prices shown do not include commissions, fees, taxes, maintenance, insurance, etc.)

|

Corvette Value Trajectory |

1963 Corvette L84 coupe |

Gain or |

2013 Corvette Z06 coupe |

Gain or Loss |

|

Purchase price |

$116,600 |

NA |

$75,600 |

NA |

|

Value in 2014 |

$129,600 |

+11.1% |

$68,375 |

-9.6% |

|

Value in 2015 |

$130,000 |

0% |

$62,700 |

-8.3% |

|

Value in 2016 |

$143,000 |

+10% |

$56,500 |

-9.9% |

|

Gain or Loss |

+$26,400 |

+22.6% |

-$19,100 |

-25.3% |

The table reveals that the 1963 Sting Ray soundly outperforms the new Stingray, gaining 22.6% in value over three years while the new Z06 loses 25.3% during the same period. Point earned for the vintage ’Vette.

Financing breeds success

Now let’s look at how much it might cost you (or reward you) on a monthly basis to collect that 1963 Sting Ray Fuelie compared with a new Z06. After all, doesn’t the world revolve around the “monthly payment”? In our example above, from 2013 to 2016, the ’63 L84 gained $733 monthly in value, whereas the new Z06 lost $531 per month. Yikes! That’s a $1,264 per month advantage for the ’63.

A standard financial strategy is to finance (buy) an appreciating asset and lease a depreciating one. Since the ’63 is more like the former than the latter, buying makes sense.

But here’s where the trail toughens, because had our fictitious buyer financed the entire cost of that Split-Window at a typical classic-car rate of 5.5% interest over three years, the monthly principal and interest payment would be a whopping $3,521. That’s like shouldering a second mortgage in a nice ZIP code. Not cheap! (In contrast, financing the 2013 Corvette Z06 at a new-car rate of 2.99% for three years would cost $2,198 per month.)

|

Finessing |

1963 Corvette L84 coupe (financed at 5.5% over 3 years) |

2013 Corvette Z06 coupe (financed at 2.99% over 3 years) |

|

Monthly payment, principal and interest |

$3,521 |

$2,198 |

|

Interest paid over 3 years |

$10,150 |

$3,535 |

In further detail, the total interest paid on the 1963 Sting Ray loan over three years totals $10,150, so in our case study, the old car’s appreciation handily outstrips the cost of financing it. When insurance and upkeep are factored in, the L84 might thus be a break-even buy or even better, meaning that after three years of fun, you could walk away with all your money.

I will readily admit this is the simplest of examples that does not reflect variations in insurance, registration or maintenance costs for old versus new cars. Most especially, it rather assumes the best-case scenario for the collectible car, since 1963 Sting Rays — in particular Fuelies — have been on a tear of late. But it’s a start.

Dare to compare

As they say, aim to succeed but prepare to fail. So what happens to our pie-in-the-sky 1963 Corvette investment scenario if the market tanks like it did in 2009? Back then, the squawking magpies were all frozen on the powerlines, afraid to bail in fear of losing capital and afraid to buy in fear of the market dropping further.

So let’s say the economy shakes, rattles and rolls downhill this fall, around election time, and that the $143,000 Sting Ray you have just married over the July 4, 2016, holiday loses 20% to 30% of its value over the coming three years instead of posting a gain? Could happen.

In this less-pleasant scenario, by 2019, the same Sting Ray would post a three-year loss of $28,600 to $42,900. On top of the 5.5% interest ($12,449) you’ll have paid, that nets an Advil-headache-case-scenario loss of $41,049 to $55,349 over the three years.

Despite this collector calamity, surprisingly, the loss is consistent with the projected $41,463 worth of depreciation and interest paid for our new 2013 Z06 over the same period. So even in a real downturn for the Sting Ray Fuelie market, your exposure above and beyond that of purchasing a new car is minimal.

The takeaway

Where does this all leave us? According to our findings, buying a new Corvette Z06 will result in significant value loss, almost guaranteed. Whereas investing in the right used Corvette — Sting Ray Fuelie or otherwise — may make you money, recapture your investment, or else in a down market, leave you on par with a new car or slightly below.

The outcome depends on many variables — only some of which can be controlled.

Because of this, many investments (e.g., stocks, timeshares, gold mines or some barn-find dragster) are something of a gamble. But at day’s end, vintage ’Vettes aren’t a blind wager like nickel slots, because through study, you can learn and neutralize many of the factors that can bite, bettering your odds of success.

See? Corvette collectors are not illogical at all. We’re just psycho-logical.